Experts' Quotes

“The most important takeaway from the Budget, was a tax that did not materialize i.e. no inheritance tax was proposed. There were several important changes on the tax front, including several clarificatory provisions and an expansion of select incentives. There were also very far-reaching announcements with regard to foreign investment regimes and a proposal for considering an increase in limiting promoter shareholding in listed companies.

On the tax front, rates did see some changes both for individuals and for corporates. For individuals with incomes in excess of Rs. 2 crores and Rs. 5 crores, the rates will see a significant increase (of 3% and 5% respectively), which takes the top bracket to around 42%. While tax rates in the 40s are not unheard of globally for individuals, it should be noted that in the absence of a strong social security system in India, these rates may be considered quite high. For corporates, the threshold for qualifying for the reduced rate of 25% has been increased from Rs. 250 crores to Rs. 400 crores. This is of course a very welcome move, and a step in the right direction.

An expansion of tax incentives to International Financial Services Centres and for the promotion of affordable housing demonstrate the continued priority that the Government is attaching to these areas. Perhaps mindful of the stress in the Non-Banking Financial Company sector, provisions have been made to give them greater parity in tax treatment with scheduled banks. Start-ups too saw several favourable changes, both in the context of the so called ‘angel tax’ provisions as well as loss carry forward provisions.

There are several measures proposed for promoting a cashless economy, the most significant of which is a 2% TDS levy on cash withdrawals in excess of Rs. 1 crore in aggregate in the year. Other important changes include an expansion in the scope of buyback tax to include listed companies as well as clarificatory amendments relating to secondary adjustments and the mode of assessment of modified returns filed pursuant to an APA.”

- "A Budget focused on redistribution of wealth with tax administrative reforms keeping in mind increased digitization of transactions.

- The Dispute Resolution and Amnesty Scheme for erstwhile indirect tax laws covering excise duty and service tax is attractive as it gives a one-time opportunity to settle all past disputes irrespective of the appellate forum the dispute is before. It gives immunity from penal interest and penalties.

- Liberalization of FDI in areas on aviation, insurance intermediaries and relaxation of single brand sourcing condition shall attract investments. This coupled with increase in FPI investment limits is expected to boost foreign exchange reserves, besides creating new avenues for growth and employment.

- No major policy shifts in direct taxes such as introduction of wealth tax or inheritance tax, which was feared by the markets. Instead, in addition to, surcharge on income tax of 25% (for income between 20 and 50 million rupees) and 35% (on income above 50 million) has been introduced as a revenue mobilization measure.

- Inverted duty structure has been addressed for a host of industries by tariff mechanisms to levy an enhanced customs duty on finished goods and reduced duty on raw materials. This will encourage domestic manufacturing and promote Make in India programme.

- Angel tax issue has been addressed in its entirety with no questions asked on valuation of shares issued to investors."

“The effort for resolving pending service tax and excise cases is commendable. The rigor of withholding tax for payers seems to continuously increase year on year. While bringing more filers into the net may be the objective, this increases the costs of doing business and makes payers liable to penalties and in some cases prosecution.”

"The FM has presented a budget that is pragmatic and reflects the economic realities facing the nation.

On the macro front, the capitalization of banks and increased allocation to infrastructure should provided am impetus to the growth aspirations laid out by the government. The announcement with regards to proposed increase in minimum public shareholding in listed companies should be treaded with caution and should not result in forceful sale by promoters. Extending the 25% corporate tax rate to companies with less than turnover of INR 400 Crs is certainly a move that corporate India would cheer about and the non - applicability of Angel Tax upon declaration, extension of relief to Category – II AIFs and setting up of a separate cell to Start- Up’s is a welcome step. A increase in FDI Caps for Insurance intermediaries from 49% to 100%, Proposed easier sourcing norms for Single Brand Retail and intent to relook at increasing the limits to Aviation, Insurance and Media augurs well for the respective sectors.

On the personal tax front the move to tax the super rich by way of an additional surcharge would make them less richer but the move to refrain the introduction of the Inheritance tax is a welcome step.

The Budget is largely a ‘promissory’ in nature with a lot of policy reforms that would be formulated in the coming days. The expectation now would be on the relentless execution of the announcements coupled with agile policy making that enables course correction when needed to put the Indian economy on the path of sustained growth."

"As was widely expected, the Finance Minister has laid down a medium term road map for jump starting the Indian economy towards the goal of reaching $5 trillion in the next few years. Towards this objective, there have been some far reaching policy announcements including proposals for developing rental housing while leveraging public sector and government land assets through the Public Private Partnership (PPP) model, deepening of long term bonds markets and liberalizing investment norms by Foreign Portfolio Investment (FPI) in certain kinds of bonds, creation of a social stock exchange in social enterprises, further liberalizing of Foreign Direct Investments (FDI) into aviation, media and insurance intermediaries, relaxation of local sourcing rules for foreign companies engaging in single brand retail. Similarly, the announcement for further capital infusion of Rs 70,000 crores in public sector banks and partial credit guarantee by Government of India for purchase of high rated pooled assets of financially sound NBFCs by PSBs for well runs NBFCs are attempts to address some of the financial stress in the economy which has arguably led to lesser private sector investment. However, India Inc may be disappointed at relative lack of specific measures to further stimulate demand in the economy. Whilst the promised reduction in the corporate tax rate of 25 percent has now been extended to many more companies (with the turnover limit upto Rs 400 cores), the reality is that it is the large companies which have a great contribution to the overall economy and they are still taxed at the higher rate of 30 percent. Considering the fact that there has been a fairly steep increase (upto 7 percent) in the maximum marginal rates of taxation at higher income levels, and that no visibly meaningful reduction is proposed in indirect tax rates, it seems that the desired push for consumption may not be seen.

There are some far reaching steps on the technology enablement measures in this Budget, for eg, the acceptance of Aadhaar as the single identity proof for tax purposes, the transformative introduction of pre filled tax returns with data available with the government, piloting e- assessment for certain taxpayers with absolutely no need of human contact, discouraging cash transactions by introducing TDS on high value cash withdrawals from banks, elimination of transaction fees for digital payments, and further streamlining of electronic filing under the GST law.

All in all, some of the policy measures announced would certainly go a long way in removing current challenges on financing faced by businesses and also increasing economic activity especially in areas of construction and manufacturing. However, in the short term till such policies get fully implemented, there is relative lack of demand stimulus which India Inc was hoping for to accelerate economic growth."

"The Budget is long on vision, but one has to see the ground level execution. Issues around tax collection, divestment, dividend from RBI and other dimensions regarding numbers and figures are crucial.

On the Direct tax front, it is very surprising that there is no reference to the impending Direct tax code, which is supposed to be presented on July 31. Also, a pattern of putting more pressure on the ‘fortunate’ sections of the society is emerging and could be a pointer of things to come; one potential dimension is the possible introduction of estate duty in the relatively near future. This is unfortunate, since it seems better to focus on growth (as the economic survey has pointed out) and look at tax collections as a consequence of growth, as opposed to looking at tax collections in isolation.

The increase in limit of turnover for lower corporate tax rates to Rs 400 cr is very welcome, and hopes that the long awaited across the board reduction happens; this will also release some funds for corporate growth.

The so called relief on Angel tax misses the key issue : Section 56(2)(viib) is an extreme case of an outlier provision, and rather than chipping away and reducing the irrationality, the section should be deleted.

Corporate restructuring is the need to be the hour, and whilst an amendment re need to account at book value (for tax neutral demerger) has been addressed (from FY 19-20), unfortunately, several representations (eg shares in subsidiary and associate companies should be clarified to be part of “undertaking”, need to broadbase loss set off in case of mergers to all assesses and not just manufacturing etc, facilitating conversion of companies into LLPs) have not been addressed."

On Financial Services: "To improvise availability of investible stock to the FPIs, the recommendation to enhance the default aggregate FPI investment limit is a welcome step. Especially as global passive funds are gaining prominence, these funds track global indices composition which, inter-alia, depends on available floating stock. Setting the default aggregate FPI limit to the sectoral limit which in certain sectors is 100 percent (as against 24 percent), this will help improvise the head room for FPIs."

On merger of NRI and FPI routes: "Presently, neither are NRIs/ OCIs permitted to register themselves as FPIs nor an entity which is more than 50% owned by NRIs/ OCIs is permitted to obtain FPI registration. There are also other restrictions on investment by NRIs/ OCIs – transactions to be pre-funded, no netting off of transactions, transaction to be executed through Category I AD banks, etc. The proposal presented for merging of the FPI and NRI-PIS route with appropriate KYC norms will provide a single route for all types of portfolio investments into India resulting in simplification and ease of doing business for NRIs/ OCIs. If implemented, this could further pave the way for majority NRI/ OCI owned entities/ funds to access the Indian markets"

“As always, the expectations from the Budget were soaring high, more particularly in case of this Government backed by a huge mandate. The budget provide much needed impetus to capital market both equity and debt. Increasing minimum public shareholding to 35% is a masterstroke but should be staggered over a time period. The relaxation of FDI norms would act as a catalyst for foreign exchange inflows. Finally, Angel tax issue seems to have been addressed and the Government has realized start-ups need to be nurtured. Also, preservation of losses in case of start ups is a well deserved incentive but could have been better. With the International Financial Service Centre on radar, the Government is looking to get the people onshore, showcasing the change in mindset, as the Government is willing to provide incentives to organization to carry out business in India and to generate employment. Overall a promising budget, looking forward to the execution plan.”

In its second term, the Modi 2.0 Government presented its first budget today. A slew of reforms were announced by the Hon’ble Finance Minister in her maiden Budget speech, revolving around infrastructure spend and boost in private and foreign investments into the economy. The key tax and regulatory measures are summarised below:

- The turnover threshold for taxing Indian companies at a lower base rate of 25% has been increased and accordingly, Indian companies whose turnover for the fiscal year 2017-18 was INR 400 crores would be entitled to be taxed at a lower rate of 25%. No changes have been proposed to the tax rates or slabs for individuals; except for increase in surcharge for “super- rich” individual taxpayers, having taxable income above INR 2 crores, with a peak tax rate of 42.74% for individuals having taxable income in excess of INR 5 crores

- With a view to provide a fillip to its objectives under the FAME scheme, the Hon’ble FM proposed several reforms for the electric vehicle manufacturing sector such as reduction of GST rate on electric vehicles from 12% to 5%; waiving off custom duty on parts used for manufacturing of electric vehicles and also providing an additional deduction of INR 1.5 lakhs under the Income-tax Act on interest paid on loans taken to purchase electric vehicle.

- The proposal to increase the minimum public shareholding in listed companies to 35% from the existing 25% is likely to create liquidity in the equity market; however, the challenges around dis-investment by promoters need to be dealt with appropriately

- In order to encourage start-up culture, the Budget proposes that start-ups and their investors will not be subject to the rigours of scrutiny proceedings with respect to funds raised by a start-up at premium; provided the necessary documentation has been submitted. Start-ups should now be able to raise capital from Category II AIF funds as well without having any need to justify the valuation.

- To address the pending legacy litigation under the pre-GST regime, a dispute resolution scheme was announced which aims at settling these long pending disputes. The FM further announced various initiatives to simplify the GST regime such as filing of a simplified single monthly return; increasing the threshold upto INR 5 Crores for quarterly filing of returns by taxpayers

- The Hon’ble FM further mentioned opening up FDI in sensitive sectors such as aviation, media and insurance; permitting 100% FDI in insurance intermediary companies

- The Budget proposes to extend benefits to IFSCs by extending tax holiday to an IFSC unit to 10 years; removal of DDT on dividends distributed by an IFSC; exemption of interest paid to a non- resident by an IFSC; exemption on capital gains to Category-III AIF investors

- While a notification in this regard is awaited, the proposed merger of NRI/ OCI scheme along with FPI scheme and permission to FPIs to investing in companies upto sectoral caps is likely to boost FDI investments into India

With the Budget announcements, a slew of reforms and policies are expected in the coming months. The Government forecasts the Indian economy to be at USD 5 Tn by 2025; while it faces challenges around growth in GDP, recovery in domestic consumption, global slowdown in FDIs coupled with trade tensions and bad loan strain on the Indian financial sector.

The first budget of the second term was focussed on providing relief to tax payers while collecting revenues from specific groups. The major relief was the reduction of corporate tax to 25% for companies with turnover upto 400 Crores. Startup are a focus for the Government. The Budget proposes simplified process, carrying forward of losses and lesser scrutiny from the tax authorities. The 2% TDS on cash withdrawal may have some legal ambiguities. The major revenue proposal is the Amnesty scheme for clearing the old cases in the legacy excise and service tax regime. Mechanism for operationalising the scheme will closely watched. Overall, a good start for the Government.

"The direct tax proposals contained in FM budget proposals are aimed primarily to achieve higher compliance, minimise cash payment and providing reliefs to Start-up and mid-market companies.

- The scope of extending buy-back tax for listed companies too is aimed at mobilising revenue but may have practical challenges on implementing it. Further the effective date of this amendment from “5th July” raises concerns for the listed companies who have already planned for buy-back.

- In the first budget presented today by the new government, the government tried to address various issues impacting various sectors of the Economy. The proposal to inject 70,000 crores into banking sector and also giving a major push for Infra project and also slew of proposals on liberalising FDI investments into Insurance, Airport and Media sector along with easing of sourcing norms for Single brand retails are welcome measures.

- The proposal by Government to launch a scheme to invite Global Companies to set up Mega-Manufacturing plants and providing them investment linked incentives under Income-tax is certainly a positive measure and I hope it gets implemented in letter and spirit.

- The proposal to increase the turnover from 250 crore to 400 crore for Corporates to be eligible for 25% Corporate Tax rate has met the demands of SME sector partially.

- Further the measures to rationalise Angel Tax for Start-ups through disclosure norms and also facilitating carry forward of tax losses for Start-up companies due to change in shareholding will augur well for Start-up. This is a step in right direction to create more positive environment for functioning of Start-ups in India.

- The government aims to promote cash less economy by encouraging electronic or digital payments. Hence the imposition of 2% of TDS on cash withdrawals of more than one crore is a step in the direction of ensuring cash less economy. Further in the absence of consequential amendment under section 199, the availability of this TDS as a credit is a matter of debate and it may become cost for the tax-payers who are withdrawing more than 1 crore.

- Further bringing of “gift” between unrelated party under the charging section 9 may impact restructuring proposals which involves transfer of shares under contribution method or for “no consideration”. However the taxability of this transactions is subject to DTA provisions and if the same is not subject to tax under “other income” clause of DTA provisions, the DTA provisions will prevail.

- Expanding the scope of TDS obligations on Individuals/HUF for payments made in excess of Rs 50 lakhs to professionals and contractors though aimed to improve compliance but imposes compliance burden on Individuals.

- To sum up in one line “ Well intended with clear statement” and hope it gets implemented in letter and spirit."

"Forward and Backward Budget !

Having done pioneering work in GiftCity, Start-up, Venture capital and social stock exchange arena, it was nice to hear favourable changes but devil lies in detail. On the negative side combined with dividend distribution or share buyback tax, effective personal rates could be about 50%. While many breathed a sigh of relief when they did not hear about reintroduction of estate or wealth tax but there is no comfort it would not happen. There seems to be a a socialistic trend to the budget."

"Hon’ble Finance Minister Sitharaman’s maiden budget and policy statement is a sincere attempt to put India on the Growth Path to become a USD 5 Trillion Economy.

Key Policy Announcements include overhauling India’s antiquated and numerous labour laws and consolidating them into just four new codes, recapitalization of Public Sector Banks with INR 70,000 Crs in the current fiscal, thrust to the rural economy with ambitious plan increases to affordable housing, upgradation of roads and solid waste management, rebooting Public Private Partnership in Railways and other sub-sectors and an overarching amount of INR 100 Lakh Crores to be invested in Infrastructure Sectors over the next 5 years.

Direct Tax proposals did not see any material changes. Extension of lower Corporate Tax rate of 25% to companies with turnover upto INR 400 Crs, extending few sops to Start-ups and levying a sharply increased surcharge for those earning incomes in excess of INR 2 Crs and 5 Crs were highlights. There was however a clear push towards electronic interface between the Tax Department and the taxpayer, with even an electronic pre-filed Tax Return proposed by Govt. using the vast amounts of data at it’s disposal. On the Customs side, there was a slant towards protectionism, with rates seeing a hike for many commodities. There was also an announcement of a Scheme to resolve legacy disputes under the pre-GST regime.

Fiscally though the intent is to reduce the Fiscal Deficit to 3.3% of GDP, this is predicated on high disinvestment revenues and continued buoyant tax collections. The key to success will be diligent implementation of the good intentions."

"Budget 2019 by Modi Government 2.0 has touched upon very pertinent aspects of the Indian Economy, taxpayers, environment in which businesses are operating and what immediate steps are necessary to get things back on track to achieve growth objective of India becoming a USD 5 Trillion economy.

From a tax and regulatory perspective, some of the policy/ tax measures announced are geared keeping in mind the key immediate requirements for the economy:

1. FDI in Retail

Local sourcing norms to be relaxed for single brand retail.

2. International Financial Service Centres (IFSC)

Several measures from tax perspective announced to encourage new investments in IFSC. Eg: If mutual funds relocates in IFSC, no additional tax to be charged on income distributed to Non-resident unit holders fulfilling conditions; Under Sec 80LA profit linked deduction be 100% for 10 consecutive years to be selected out of 15 years; No DDT on company operating in IFSC from our of its accumulated income after a April 2017.

3. Incentives for affordable housing to boost Real Estate Sector; Deduction under Sec 80EEA upto Rs 1.5 Lacs on interest paid to enable home buyers to access low cost funds. Also deduction under Sec 80IBA (100%) on profits from eligible projects.

4. Measures to enhance digital payments and curtail cash transactions (there is a TDS @ 2% proposed for cash withdrawals from banks beyond Rs 1 Crore).

5. Aligning Sec 43D to charge tax on interest on sticky loans hitherto applicable to banks and specified financial institutions to now apply to regulated NBFC so as to provide a level playing field for them.

6. Extending the benefit of the lower corporate tax rate of 25% to companies having turnover of less than 400 crores as against 250 crores.

Also, some of the current issues with regard to fair market value of shares resulting in taxation under Sec 56(2)(x) or enhanced taxation under Sec 50CA of the Act for sellers for certain categories of transactions is also sought to be addressed. (Board is empowered to prescribe transactions to remove hardship).

A far-reaching amendment under the heading of strengthening Anti-abuse measures in Sec 115QA (ie. Buy-back tax) to be made applicable to listed shares needs to be taken notice of as it is sought to apply from 5 July, 2019.

Overall, the FM has while looking at revenue generating measures has taken some steps to improve Economic growth, address sectors ailing economy like Real Estate, announced several big-time infrastructure developments and associated fund raising plans. Surely, the space is full of action to keep watch in next 2/3 years to see how its implementation helps India achieve its USD 5 Trillion economy objective."

Co-Author: Sapan Choksi, Manager, EY

"With DTC just around the corner, Budget 2019 was not expected to carry any major changes re: TP. However, surprisingly, it did! There are two main TP related changes besides a couple of minor ones:

1) Secondary Adjustment provisions have been rationalised:

a) one-time charge of tax @ 18% + surcharge @ 12% is provided as an option to the taxpayer, as against perpetual interest imputation on cash not brought into the country following a TP adjustment

b) applicability to first year, i.e., FY 2016-17 rationalised to have either Secondary Adjustment or a similar impact agreed as part of the APA for that year

c) the cash on account of Secondary Adjustment can be remitted from any Associated Enterprise

2) Master File requirement made applicable to all Constituent Entities irrespective of whether there is any international transactions or not, as against the current provisions which applies only in cases having international transactions beyond certain threshold

The first change is extremely welcoming as it eases the burden on taxpayers in complying with the current provision from practical perspective at a one-time cost.

The second change, on the other hand, is quite puzzling as to what is the Tax office’s thinking on significantly widening the net for this compliance requirement - needless to state that it will add to significant compliance burden for the taxpayers!

We hope that the Government considers various recommendations provided over time, such as rationalising compliance requirements, block assessment for TP, rationalisation of the safe harbour rules, reduction of litigation, etc., as part of the impending DTC."

"The Hon’ble FM made a successful attempt in laying out the vision of the current government through this budget with emphasis on hard and soft infrastructure and several other measure which are inclusive in nature covering every segment of society and business. I hope to see the fine print as a roadmap for the next five years on each of these areas. On tax front, as expected, there were limited proposals, with new tax code around the corner. Proposals to remove challenges around angle taxation and ease of doing business are a welcome move. It would have been good see the proposal to reduce the overall tax rate for the companies with a turnover of more than INR 400 crores as we need to competitive on the corporate tax front with many of the countries in the region"

"The Finance Minister unleashed a pro-development budget with the ideology of “reform, perform and transform” several key sectors and geographical regions, with special focus on housing sector, electric vehicles, infrastructure development, education and relaxation of FDI in various sectors.

Some of the key Direct Tax proposals are as under:

- Rate of surcharge enhanced for individuals having taxable income from 2 crore to 5 crore and 5 crore and above, such that their ETR shall increase by 3 % and 7 % respectively

- Reduced corporate tax rate of 25% to apply to companies with annual turnover of up to Rs 400 Crores

- Significant boost provided to use of clean energy by providing investment linked exemptions to certain businesses under Section 35AD, and by granting additional tax deduction to customers of Rs. 1.5 lakhs on interest paid towards loans taken for purchase of electric vehicles

- Impetus provided to entrepreneurship seeded in young minds by introducing following measures, resulting in growth of start-ups:

-Angel tax issue resolved for investors filing requisite details as such start-ups shall not to be subjected to questions on receipt of share premium

-Providing relaxation in carry-forward and set-off of losses

- For realization of goal of “Housing for All” by 2022, enhanced interest deduction of upto Rs. 3.5 lakh on funds borrowed for purchase of affordable house provided

- Tax deductibility of interest on bad debts allowed to NBFC, to bring them at par with scheduled banks

- With a view to further incentivizing the IFSC, several direct tax incentives provided such as 100% profit-linked deduction under section 80LA, exemption from DDT, exemption from capital gains arising to AIF-III and interest payment on loan taken from non-residents

- In order to widen and deepen the tax base use of Aadhar for undertaking Income-tax compliances in absence of PAN, permitted

- Making available pre-filled ITRs and launch of faceless assessments to be monitored through a Central Cell, to curb tax evasion and certain undesirable practices on part of tax officials

- With the intent to promote digital payments and a less-cash economy, measures such as TDS on annual cash withdrawals exceeding Rs. 1 crore for making business payments introduced

- Tax to be deducted by individuals and HUFs at 5% on payments made by them above Rs. 50 Lakhs to contractors and professionals

- Gifts made by resident to non-resident henceforth, shall be deemed to be income arising in India, subject to exemption under Section 56 and applicable DTAA

- Aggregate amount of unabsorbed depreciation and brought forward business loss permitted to be reduced in cases of certain distressed companies for calculating book profits for levy of MAT

- Provisions of Section 115QA, pertaining to tax on buy-back of shares, extended to listed companies

Some of the key Indirect Tax proposals are as under:

- An amnesty scheme introduced for resolution and settlement of legacy cases of Central Excise and Service Tax

- Electronic invoice system to be introduced from January 2020 to phase out need for a separate e-way bill and also significantly reduce the compliance burden of the tax payer

- Simplification of GST compliance intended by introduction of a single monthly return and single tax ledger

To conclude, the Budget all-in-all has been a pro-reform budget, with slew of measures for the common man, the MSMEs and also the corporates. It is aimed at giving a boost to investments and growth of the economy and help India achieve its objective of becoming a $5 Trillion economy."

"The Union Budget 2019-20 is presented at a time of a slowdown in the global economy with the growth of world output falling from 3.8% in 2017 to 3.6% in 2018. Growth of the Indian economy also moderated in 2018-19 to 6.8%, lower than 7.2% in 2017-18. Yet, India continued to the fastest growing major economy in the world. In this backdrop, the Government has set an ambitious target of making India a $5 trillion economy by 2025. This calls for some bold and radical reforms. The question foremost in the minds was whether the Finance Minister 2019-20 Budget would provide a road map for this target. At this same time, while the Finance Minister was not expected to propose any fundamental tax reforms in view of the impending Direct Tax Code, there was still some unfinished agenda arising from recent legislative changes which needed to be addressed in the 2019-20 Budget.

In the 2015 Union Budget the Finance Minister had announced a phased reduction in India’s corporate tax rate from 30% to 25%. This was followed up with a 25% tax rate for newly formed manufacturing companies and for small and medium enterprises in subsequent Budgets. While the business community still eagerly awaits an across the board rate reduction, the Finance Minister needs to be commended for widening the coverage of small and medium companies to include companies with turnover of less than 400 crores.

Provisions relating to secondary adjustment was introduced in the transfer pricing law by the 2017 Union Budget. The proposals in the Budget to amend certain aspects of these provisions is welcome. The amendments seek to achieve the following: (1) protecting Advance Pricing Agreements (APAs) that were signed prior to the introduction of the provision; (2) an option to remit or not to remit the amount of primary transaction is provided to the taxpayer. In case where taxpayer opts not to remit, the taxpayer would need to pay a tax of 18% on the amount.

Overall, the Budget continues in the direction of the earlier budgets of the NDA seeking to broaden the tax base, reduce tax rates in a gradual manner, minimize opportunities for tax base erosion and enable a friendlier tax administration. The business community now eagerly awaits the Direct Tax Code and expects that the draft would be put out soon for public consultation before the same is finalized."

The union budget speech carries some incrementally helpful tax proposals but roadmap towards a moderate tax regime in the years ahead could have provided predictability. The recognition that foreign capital flows need to be encouraged and simplified is welcomed, including the attention to address issues of angel taxation. Well balanced budget given the prevailing external environment of global slowdown.

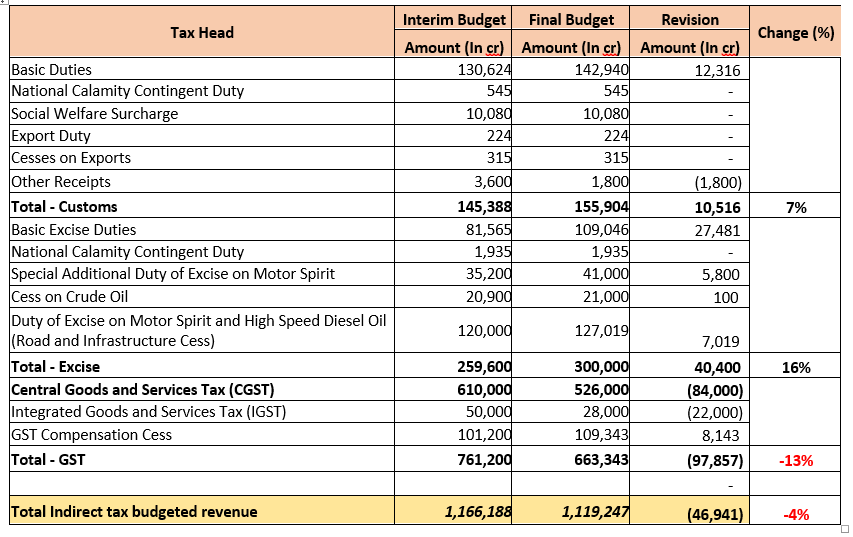

"Key proposals in indirect taxes

1. Revision in projected GST collections for FY 19-20

The government has tampered down the revenue collection target from Indirect taxes. The budgeted revenue of Central GST has been reduced from INR 6.10 lakh crores to INR 5.26 lakh crores, a reduction of INR 84,000 crore which is almost 14% of the original budgeted collection.

The government has however increased the budgeted revenue from Excise duty by INR 40,400 crores to bring up the revised target to INR 3 lakh crores. To garner this increased revenue, Excise duty rate on cigarettes and certain other tobacco products have been increased.

Similarly, the government has increased Customs duty rate on various finished products to meet the revised budgeted revenue of INR 1.56 lakh crores, an increase of INR 10,516 crores from the original revenue target of INR 1.45 crores.

As a result, the total indirect tax budgeted revenue has been reduced by 4% to bring it down to INR 11.19 lakh crores from the original budget estimate of INR 11.66 lakh crores.

Source: Budget documents

Comment

The reduction in GST budgeted revenue by about 14% seems to be driven by revenue collections in first two months of the financial year and the revised numbers look much more realistic. However, to bridge this deficit, tax rates under Excise and Customs have been increased in some cases.

Industry would hope that with revision in GST collections, the audits and scrutiny may not be as frequent and rigorous as was being feared earlier.

2. Customs update

To encourage Make in India, Basic Customs duty has been increased on gold, precious metals, buses / trucks and many automobile parts, indoor and outdoor units of split air conditioner and many electronic items. At the same time, customs duty has been reduced on inputs or capital goods used to manufacture CRGO steel, specified electronic items like Camera module for cellphones, etc.

Further, numerous steps have been taken to improve compliances and to check fraudulent availment of export benefits. These include verification of Aadhar or any other identity and provision for arrest of a person who has committed the offence outside India and making certain offences cognizable / non bailable such as fraudulent availment of duty scrips, duty drawback etc. Penal provisions have become more stringent with increased amount of penalty in specific cases.

3. Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019

A dispute resolution scheme has been proposed to settle pending litigation under Excise, Service tax and many various other cesses & levies (of pre GST regime). This scheme covers all cases pending before any appellate forum (including Tribunal, High Court, Supreme Court) and provides for relief ranging from 40 to 70% of tax dues, including interest and penalty. It has been mentioned that more than 3.75 lac cr is blocked in litigation in service tax and excise laws.

Comment

This is a great initiative by the Government, as the industry is looking to move on after implementation of GST. Given the quantum of relief, the scheme looks very attractive and may get encouraging response from industry. It could garner additional revenue for the Government and also help the industry to have increased focus on GST related proposed changes such as E invoicing, new compliance framework etc.

Overall comment

Indirect tax proposals are based on promoting the key themes around make in India, environmental concern, technology led tax administration and ease of doing business. Implementation of E invoicing from Jan 2020 will give time to the Government as well as industry to prepare. Customs duty rates have been reduced on many inputs to incentivize manufacturing and increased on finished products to garner additional revenues as well as to reduce non essential imports. Proposal to introduce legacy dispute resolution scheme for pending litigation is also a great idea and should help the industry to move on with GST in place. Interest subvention for GST registered MSMEs should help in expansion of tax base while reducing the cost of doing business."

"The Tax Proposals in this budget are well thought out and are clearly based in various representations.Examples include relief to start ups,parity in tax treatment for NBFC,increase in coverage of companies under 25%rate,amendmnt to Section 50 of CGST to levy interest only on tax paid through cash ledger and the Legacy Dispute Settlement Scheme"

"The budget speech by the Finance Minister was unique for the reason that it deviated from the long standing practice of highlighting the thrust areas for tax proposals, nor did it spell out what the proposals entail by way of revenue gains or revenue losses.

Coming to the indirect tax proposals the Finance Minister did lay down certain objectives for customs proposals but certain spelt out objectives such as securing borders are conspicuous by its absence in detailed proposals, the proposed amendments being more in the nature of penal provisions for offences. The WCO theme of the current year of ‘smart borders for seamless trade’ required concrete steps to reduce trade frictions.

In hiking duty on gold and precious metal, did the Government fail to appreciate that imposition of lower tax rates encourages better tax compliance? We had witnessed significant transparency and tax compliance when the BCD was at 2% and VAT at 1%. The World Gold Council estimates that the smuggling of gold has significantly increased in the past years since the BCD was hiked to 10% and the grey market will thrive and dilute efforts on reducing cash transactions.

The excise duty and cess on petrol and diesel have been hiked. But coming in the wake of lower crude prices and also a steady rupee, one should hope that the increase which would be immediately effective would not be passed on in its entirety.

The move to introducing a dispute resolution scheme is not an unexpected move. But the devil lies in detail. Prima facie, the provision which indicates that the amount of pre deposit paid during enquiry, investigation or audit or at any stage of appellate proceeding are not to be reduced while arriving at tax dues but should be adjusted against the amount payable is welcome. But then why not refund any amount so deposited that exceeds the amount payable? The provisions are also silent on adjustment, if any, of the refund due to the declarant.

Overall, one cannot say that the budget has provided any policy direction or acted as a tool for economic impetus except to a limited extent of duty rate adjustments in the hope that they will lead to success of Make in India."

"After presenting the Economic Survey yesterday, the Hon’ble Finance Minister Ms. Nirmala Sitharaman today presented the Modi Government’s first budget in the second term. The Budget focused on major structural reforms and incremental policy initiatives.

The Budget has touched all the sectors and areas ranging from the aspects affecting and impacting the common man to promoting start-ups and entrepreneurship skills, to provide ease of doing business environment to the SME and MSMEs and focus on areas of socio-economic relevance like education, infrastructure (airways, roadways, waterways), water management, electrification of rural households. A lot of emphasis has also been given to the affordable housing and various incentives have been proposed on this front. A special effort has been made to bring major structural reforms to banking and financial services sector, this is a very welcome initiative considering the recent issues in the banking sector. The budget has specifically laid down the roadmap to empower and grow the PSU banks.

The major direct tax and other regulatory reforms have been summarised below:

Corporate Tax:

The Budget proposed to provide relief to corporates, by increasing the turnover threshold from INR 250 crores to INR 400 crores for applicability of lower corporate tax rate of 25%. It is worth noting that the benefit shall be applicable from Financial Year 2019-20 itself. It may be noted that the LLP continues to remain taxed at 30%.

Investment linked deductions u/s 35AD have been proposed for global companies setting up mega manufacturing plants in sunrise and advanced technologies areas. Eligible assesses setting up their units in the GIFT city have been granted a 10 year out of a block of 15 year window to claim 100% profit linked deduction. These measures alongwith other initiatives are bound to generate employment locally.

The scope of buyback tax has been proposed to be extended to shares of listed company as well.

In order to further facilitate ease of doing business in the case of an eligible start-up, it is proposed to amend section 79 so as to provide that loss incurred in prior year (in the case of closely held start up), shall be allowed to be carried forward and set off against the income of the current financial year on satisfaction of either of the two conditions as stipulated currently at clause (a) or clause (b) thereunder.

Insofar as the transfer pricing is concerned, it has been proposed that the taxpayer can pay additional tax @ 18% (plus 12% surcharge) on such ‘excess money or part thereof’ not repatriated within the prescribed timelines and such payment of taxes would be considered as final payment.

In order to bring within the tax ambit, the gifts made to person resident outside India, it is proposed that such gifts shall be deemed to accrue / arise in India thereby widening the scope of section 56. However, the exemptions provided under section 56 (including the definition of the term ‘relative’) will continue to be applicable.

Angel Tax:

The Budget also provided a long sought relief to the pending litigation on the issue of Angel tax. The Hon’ble Finance Minister has assured the community that the registered start-ups would not face scrutiny from the income tax department especially in areas relating to valuation of shares, etc. As regards the issue of the identity of the investor and source of the funds, it has been proposed to put in place a mechanism of e-verification.

Individual Tax:

The surcharge rate for “super-rich” individuals has been proposed to be increased from 15% to 25% (if income is between INR 2 to INR 5 crores) and to 37% (if income exceeds INR 5 crores). The effective tax rate will accordingly go up by 3% and 7% respectively for such individuals. For the common man, various incentives like the benefit of additional deduction of INR 1.5 lakhs on interest for loan to buy a house under the affordable housing scheme has been proposed. Similarly, interest paid on loan taken for purchasing electric vehicle allowed as a deduction, etc.

No mention / reference has been made to introduction of inheritance tax.

Tax Administration:

In order to ease the taxpayer’s compliance burden, the tax department has proposed measures such as pre-filled income tax return, interchangeability of PAN and Aadhar, faceless e-assessments, single point of contact cell for scrutiny assessments. Further to boost reduced use of cash in the system, it has been proposed to levy a TDS @ 2% on cash withdrawals in excess of INR 1 crore in a year. Also, proposes that specified business establishments shall offer digital payment mode to customers at no cost.

Other major regulatory reforms:

The budget has brought about regulatory reforms as well. The foreign exchange liberalisation continues as the Hon’ble Finance Minister relaxed the FDI limits in specific sectors including aviation, insurance intermediaries and single brand retail. Further to ease the FDI flow, FPI route and the NRI-PIS route have been merged. FPIs will also be permitted to subscribe to listed debt securities by ReITS and InvITs.

Lastly, the Hon’ble Finance Minister, ended her speech stating that the fiscal deficit has been reduced from 3.4% to 3.3%. Overall, one can say that the budget has largely met the expectations especially when it comes to areas like ease of doing business, make in India and digital India, boost to start-up and entrepreneurship, infrastructure and housing for all and socio-economic sector (including sports and yoga)."

"The first budget of Modi Government 2.0 announced various proposals including a thrust to promoting a cashless economy, incentivizing inbound investments into India, a focus on electric vehicles and reducing the pendency of tax litigation. The key highlights of the budget are a significant increase in the rate of tax for high income earners, increase in the excise duty on petrol and diesel and the introduction of legacy dispute resolution scheme.

While it was expected that there would be very few Indirect tax proposals as part of Union Budget post GST implementation, however, there are quite few proposals to promote Make in India. Some of these measures will have a far reaching impact on the economy. The introduction of dispute resolution scheme is the most welcome announcement which gives an opportunity to tax payers to amicable settle the dispute. The relief provided under the scheme is very lucrative for the tax payer to opt under a scheme to avoid long drawn litigation. Overall, being the first budget, the Government has clearly laid down the path both for simplification of tax regime and incentivising future technology. Surprisingly, there is no mention of the Direct Tax Code."

"India has emerged a global financial elite and the Finance Minister herself has enunciated India’s economy to be the sixth largest in the world. Considering, the direct tax revenue, which has increased by over 78% in last 5 years, not many changes have been proposed in the individual tax slabs for individuals. However, the super-rich will have shell out an additional tax in the form of enhanced surcharge. A surcharge of 25% on those having total income exceeding 2 crores and upto 5 crores and those having income more than 5 crores shall have to bear an additional surcharge of 37% of the income tax. This is a move in the right direction, the government has rightly abstained from introducing an Inheritance tax and contained its revenue need by taxing the super riches of India.

Removal of cumbersome processes, rationalisation of the tax rates, digitisation, and promotion of cashless economy has always been a matter of precedence for this government. In pursuance of this concept “faceless and nameless e-assessment” shall be launched in a phased manner. E-assessments shall be carried out in cases requiring verification of certain specified transactions or discrepancies, and notices shall be issued electronically without disclosing the name, designation or location of the Assessing Officer. Apart from saving time and costs, this measure would bring in more transparency and reliability in the Indian Taxation System.

Additionally, pre-filled Income Tax Returns shall be made available to taxpayers, comprising details of salary income, capital gains from securities, bank interests, dividends and tax deductions obtained from sources such as Banks, Stock exchanges, mutual funds, EPFO, State Registration Departments etc. Apart from reducing the time taken to file tax returns, this move shall also ensure precision in reporting of income and taxes.

Standing by its promise the government has further widened the ambit of the companies eligible for the lower rate of tax of 25% which is currently applicable to companies having annual turnover up to 250 Crore, by extending the benefit of lower rate to all companies having annual turnover up to 400 crore. A remarkable 99.3% of the companies will enjoy the benefit of the reduced rates.

Digital India being a flagship programme of the government, in its second term the government has taken a step further in promoting digital payments. Merchant Discount Rate (MDR) charges have been waived on cashless payments and 2% TDS has been imposed on withdrawals of Rs 1 crore, in a year, from bank accounts for business payments, thereby discouraging cash transactions and encouraging digital mode of payment.

For realisation of government goal of “Housing for all” more tax deduction has been offered for people buying houses. Additional deduction of Rs. 1.5 lac has been proposed for loan taken to buy affordable houses having stamp duty value upto Rs. 45 Lakh. This shall not only provide impetus to the real-estate sector but also ease the tax burden of the middle class society of India and help them achieve their dream of owning a home.

In order to incite the start-ups and resolve the ‘angel tax’ issues, start-ups and their investors who provide requisite declarations in their returns will not be subjected to any kind of scrutiny in respect of valuations of share premiums. In addition, special administrative preparations have been proposed to be made by CBDT for pending assessments of start-ups and for the redressal of their grievances. Moreover, valuation of shares issued to Category II Alternative Investment Funds (AIF) shall now be beyond the scope of income tax scrutiny. Presently, only Category 1 enjoys such leeway.

Reduction of tax rates for small companies, simplification of procedures, promotion of start-ups in the form of tax incentives are among the few things the government has always sought to provide and it wouldn’t be wrong to say that it has been successful to a great extent. Budget 2019 proves that the government shall continue to work toward creating a tranquil, non-adversarial tax regime for the taxpayers."

"As expected, the budget was more of laying down of the vision of the Government over the next five years and the income tax proposals also were more on the lines of rationalisation measures and measures to widen the tax base. One hopes the increased surcharge for individuals and HUFs is only temporary as firms and companies have been spared therefrom. The proposal to reduce the corporate tax rate to 25 percent for domestic companies having a turnover of less than Rs. 400 crore in the financial year 2017 -18 is welcome. As expected, there was no levy of inheritance tax or any major amendment in the capital gains taxation though the proposal to levy tax on buy back of listed shares does take one by a mild surprise, as does the proposal to tax non residents on gifts received outside India from resident non relatives. Many proposals discourage usage of cash and encourage use of digital payments which are generally welcome. There is a proposal to give a deduction of upto Rs. 1.5 lakhs on interest paid on a loan borrowed to buy an affordable house or buy an electric car. Hopefully one will have adequate infrastructure to ply an electric car in India soon.

These are proposals to simply a taxpayers life like introduction to pre filed returns, faceless e-assessments and Aadhar PAN interchangeability which will need to be tested in terms of their efficient functioning. Like the Dispute Resolution Scheme of legacy indirect tax litigation when the Government enacts the new Direct Taxes Code, it may want to consider a similar scheme at that time. The transfer pricing related proposals are more in the nature of rationalisation / relief. Overall, the proposals are not in the nature of major policy related shifts."

"Given the economic conditions, sluggishness in job data, low demand in auto sector, it was expected to be a big bang budget by Modi 2.0. While the Finance Minister (FM), Nirmala Sitharaman, addressed a few important points such as vision of USD 5 Trillion economy, strengthening connectivity through infrastructure and a slew of announcements on financial markets, overall it was a lacklustre budget.

On the tax front, the most important announcement was tax on super rich which would effectively increase the rates to 42.744% for individuals earning income above INR 50 million. In our view, this may not be a logical move as we are moving towards a lower corporate tax rate regime and simultaneously imposing a higher taxes on individuals. From a global perspective, foreign countries do have higher taxes on individuals but they have a robust social security system which India does not have currently.

Other key tax amendments includes levy of buyback tax on listed companies, tax relief to start-ups, TDS on cash withdrawals above INR 10 million, inter-operability of PAN and Aadhar, implementation of faceless assessments via electronic mode, mandatory filing of returns in certain specified cases, etc. These amendments would result in higher compliances and also seek to curb tax avoidance by using cash as a mode of transaction.

One of the big set-back of this budget could be buy-back tax on listed companies. There could be a huge tax leakage for companies as buy-back tax is applied on buy-back price less issue price, irrespective of the purchase price of the shareholders. This was the precise reason why this tax was not applicable to listed company. However, with this amendment, lot of companies would be discouraged to give back the accumulated profits to its shareholders.

On Transfer pricing side, an important amendment is with respect to the provisions of ‘secondary adjustment’. With effect from 1 September 2019, the taxpayer will have an option to either bring the amount of primary transfer pricing adjustment in India along with interest, if applicable, OR pay an additional income tax of 18% (plus a surcharge of 12% on tax) without a need to bring the money into India. The additional tax is not deductible under any provisions nor any credit can be claimed for such tax. Companies can now evaluate both the options and decide their course of action with respect to the transfer pricing adjustments made.

As expected, it is clarified that the secondary adjustment provisions are applicable if either of the conditions is triggered i.e. the value of primary adjustment is more than INR 1 Crore or the adjustment pertains to AY 2016-17, and not both. This is a welcome clarification.

With respect to applicability of filing of Part A of Master file (Form 3CEAA), if other prescribed conditions are satisfied, even though there are no international transactions undertaken during the year, the constituent entity in India should file Part A of the Form. Further, the non-clarity regarding the definition of ‘accounting year’ is resolved now. The ‘accounting year’ in case of an international group, the parent entity of which is not resident in India, shall be the one applicable to the ultimate parent entity.

In addition, there are several provisions that alleviate genuine hardships. All-in-all, it’s a balanced budget but it needs to be seen how government addresses the economic slow down and growth challenges."

"The Union budget seeks to commence the new term of the government on an upbeat and progressive note consistent with the ‘Make in India’ objective and winning the confidence of the taxpayers (Sabka Vishwas).

The proposals on the customs front primarily seek to increase customs duty where the indigenous capability to manufacture the items has been developed by India. Such goods include construction materials, automobile parts and specified electronic items. Curbing non-essential imports to reduce current account deficit also seems high on the agenda with increase in duty rates on precious metals and gold. Sectors which have been provided relief are medical devices (artificial kidneys), defence and nuclear power.

One amendment which would be hugely welcomed by the industry is that the payment of interest on delayed payment of tax has been restricted only to the net tax liability payable in cash. Several writ petitions were filed or in the process of being filed by the industry on this issue. Another welcome step is the facility to transfer an amount from one head to another head in the electronic cash ledger which should end the requirement of filing cumbersome refund applications on a matter of genuine mistake on account of the taxpayers. Constitution of the National Appellate Authority for Advance Ruling should take care of the conflicting rulings of the Advance ruling authorities of two different states.

The big highlight of course has been the dispute resolution cum amnesty scheme called the Sabka Vishwas Legacy Dispute Resolution Scheme. This should have a far reaching effect in ending protracted litigations in the legacy laws and help in settlement of cases providing relief to the taxpayers as well as boosting the short term revenue collection of the government."

"The maiden budget laid out by the first women Finance Minister, Ms Nirmala Sitharaman was comprehensive in all aspects and thankfully has no surprises or significant additional burden on the taxpayer from a Transfer Pricing perspective, rather it provides clarity on crucial issues of post-APA compliance, Secondary adjustments and master filing requirements in India. There are certain important aspects explained in detail below that merit attention of taxpayers.

1. Proceedings in respect of the Modified Tax return for APA years

The Finance bill proposes a clarification with regard to the processing of the modified returns of income filed by the taxpayer pursuant to an APA. It proposes that the tax officer has to pass an order in line with the modified income pursuant to the APA and not conduct any fresh assessment / re-assessment with regard to the APA years for which the assessment / re-assessment proceedings are already completed.

This in my view, will further enhance taxpayer confidence in the APA program as it tries to allay the fears of the taxpayers that the existing provisions in relation to the completed years of assessment / re-assessment could be used by the field officers as a handle to make any fresh assessment / re-assessment.

2. Secondary Adjustment

There were practical issues in implementation of secondary adjustment and the proposed budget tries to provide certain measures to allay these issues.

In cases where the taxpayer could not bring in the relevant cash flow from its associated enterprise, the Secondary Adjustment provisions manifested a vicious circle of interest on interest which technically had no end.

It is now proposed to provide an alternative route to the taxpayers to avoid getting into a vicious interest cycle by making a one-time additional tax payment of 18% (excluding surcharge) on the amount of secondary adjustment. Another important step is that the taxpayer can bring in the relevant cash from any non-resident group entity, irrespective of the transacting entity.

This is indeed a welcome and much-awaited proposal which will lead to a lot of clarification on the implementation of Secondary adjustment. Having said that, the secondary adjustment essentially remains a unilateral approach and the ability to generate the relevant cash flow, the accounting, tax and regulatory provisions applicable in the host country of the paying associated enterprise (especially in case a non-transacting associated enterprise provides the cash flow) could pose significant challenges. Also, the levy of tax @18% plus 12% surcharge effectively can be considered to be equivalent to a dividend distribution tax and maybe a huge burden on tax payers, especially for the APA rollback years. However, the good part is that it is optional and not mandatory. Therefore for tax payers who would be unable to bear the financial burden they will have the option to treat the amount as loan and pay tax on the deemed interest thereon.

3. Transfer Pricing documentation consequential to BEPS Action Plan 13

The Transfer Pricing documentation requirements in India are more or less in line with the OECD/G20 BEPS Action Plan 13 on three-tier documentation except for certain additional details required to be incorporated in the Master File which are beyond the prescribed contents of the Master File per the Action Plan 13.

In this regard, the provisions for maintaining a Master File were earlier confined to entities having any international transactions. As per the Finance Bill 2019, it is proposed that the Master File will have to be maintained by any constituent entity in India – irrespective of whether it has any inter-company transactions. However, for entities which do not have any international transactions, the rigours are confined to very basic details like name and location of international group (i.e) part A offering relevant form. This is a clarification provision in my view as the heading of Section 92D stated documents to be maintained by person entering into international transaction. Now by bringing this separately under sub clause (2) of Section 92D it makes it abundantly clear.

Another important clarification is with regard to the definition of the accounting year which is now proposed to be clarified as the accounting year of the parent entity as against any other interpretation.

4. Business Connection issue for eligible investment funds

The Finance Bill 2019 in it’s bid to simplify the process for avoiding an allegation of business connection for eligible investment funds, have proposed to introduce a specific remuneration model (the nuances of which would be prescribed later) in place of the existing stipulation for arm’s length price remuneration model for the fund managers. This will hopefully (assuming the remuneration model prescribed would be based on readily available data points of the fund) lead to lesser efforts – both on the side of the taxpayer as well as revenue authorities to establish and justify any arm’s length price calculation. Interesting to note the move away of the tax authorities from the avowed internationally accepted principle of arm’s length remuneration. This may seem to be more in line with the proposed draft paper on attribution of profits to PE.

All in all, the Budget lays out a welcome tone by proposing to make only certain nudging changes that aim to build taxpayer confidence and reduce ambiguities. The overall thrust on a less cash economy and a more digital orientation is manifested in the various budget proposals including the emphasis on faceless E-assessments which is proposed to be introduced in phased manners and interchangeability of Aadhaar and PAN cards. Let us hope the government is able to reign in the “elephant” and not trample the “paddy fields”. Indeed, as the honourable finance minister laid out that, it will then be the duty of the taxpayers to “feed more mounds of rice to the elephant”."

"Hon’ble Finance Minister Smt. Nirmala Sitharaman created history by becoming the first ever women finance minister of India and presented the Budget for the financial year 2019- 20 on behalf of re-elected NDA government. In her first budget speech as Finance Minister of NDA 2 Government, from a macro perspective her speech was focused more on achievement of the NDA Government in its first tenure and its priorities and the focus area for the second term of the Government such as infrastructure development, healthcare, water resource management, Swachh Bharat, Make in India initiative/job creation and importantly driving the country towards Digital Economy/less-cash-economy. As was observed, during the first tenure of the Government constant efforts were made to increase tax revenues by levying additional taxes such as introduction of 10% capital gains tax on long term equity, increase in surcharge on high net- worth individuals, etc.

Here is a quick recap of some major amendments/announcements made by the FM from the direct taxation front:

1) At present, the lower rate of corporate tax of 25 % is only applicable to companies having annual turnover up to INR 250 Crore. It is proposed that the benefit of the rate will also be applicable to all companies having annual turnover up to INR 400 crores.

2) In order to make tax assessments hassle free/corruption free, it is proposed to launch scheme of faceless assessments in a phased manner. While such faceless assessment is surely a welcome step, It will also entail some practical challenges for the tax payers :- If tax assessment involves application of tax treaties or a debatable issue, it is not clear as to how the tax payer will have an opportunity to impress upon assessing officer merits of his case. Unfortunately, this could be a significant downside of this otherwise very positive initiative of the government.

3) To grant relief to the Indian start ups form the demons of ‘Angel Tax’, following proposals are made:

a) Start ups and their investors who have filed requisite declarations and provided requisite information in their tax returns will not be subjected to scrutiny assessments in respect of valuation of share premiums.

b) The issue of establishing identity of the investor and source of his funds will be resolved by putting in place a mechanism of e-verification. Special administrative arrangements will be made by CBDT for pending assessments of start-ups and redressal of their grievances and no inquiry can be made by assessing officer without prior approval of supervisory officer.

c) Start-ups would not be required to justify FMV in respect of shares issued to Category II AIFs.

4) In order to boost digital payments and discouraging cash payments, tax would be levied @ 2% on cash withdrawal exceeding INR 1 crore in a year from one bank account. This provision effectively marks the comeback of Banking cash transaction tax (BCTT) which was effective between 2005 and 2009.

5) Unfortunately, the government has proposed an additional surcharge on High Net worth individuals @ 25% on taxable income exceeding INR 2 crores but not exceeding INR 5 crores and @ 37% on taxable income exceeding 5 crores. It would seem that this additional significant surcharge being levied on HNIs is not rational/fair. In the later category, tax rate of such individuals would be almost at par with tax rate of foreign companies in India!!. One would think that instead of increasing tax burden on existing individuals almost every year, the more efforts should be to ensure that present base of the tax payers’ is expanded by bringing people who are earning taxable income but somehow not paying income tax/not filing their tax returns.

6) Interestingly, the Finance Bill has introduced ‘buy back tax’ on listed companies as well. Presently buy back tax applies on buy back of shares by unlisted companies as an anti-avoidance measure. This is a significant proposal for listed companies in India (sec 115QA).

7) Demerger under Ind-AS scenario – To remove difficulties in the case of a demerger where Ind AS applies, the Finance Bill provides that in a demerger, where assets and liabilities are recorded at a value different from their book value, it will still be treated as a tax neutral demerger as long as other conditions are duly met with … this is a positive change.

8) Transfer pricing – secondary adjustments: To make the provisions of secondary adjustment more effective and easy to comply with, it has been provided that the conditions of Rs 1 crore threshold and the primary adjustment made upto 1 April 2016 are alternate conditions and not to be read together. It is also provided that the excess money can be repatriated from any of the ‘associated enterprises’. And if it is not repatriated in time, the tax payer will have the option to pay additional income-tax @ 18% alongwith surcharge.

9) Black Money Act, 2015: There is a significant amendment. To effectively implement the intention behind introduction of Black Money Act, the amendment provides that this Act will apply to a person if he was a resident of India in the year in which undisclosed income/asset was acquired. In simple words, since Black Money Act applies only to a resident of India there was an unintended scope of escapement for someone who later becomes non resident and claims non applicability of BM Act on the ground that he is a non resident of India.

All in all while the Government is focussing on many significant aspects like rural upliftment, infrastructure development, quality education in India, water resource management, job creation etc, it appears to be a mixed budget with some positives and some concerns. "

"Union Budget 2019 – Focussed, robust and directional The Government marked its comeback and made its intentions clear in the Union Budget 2019. Focussed agenda, robust measures and a directional approach - these words define the Indirect Tax measures announced by the Government.

‘Focussed agenda’ of the Government has been made clear by its boost to ‘Make-in-India’ initiative and impetus to use of alternate sources of energy including use of electric vehicles. ‘Robust measures’ include increase in rate of customs duty on a number of finished products (like electronic goods, automobiles, automobile parts, paper, plastic etc.), duty moderation on various raw materials as well as exemptions granted to defence sector etc. These changes lay foundation to put domestic industry on high growth trajectory in times to come.

‘Directional approach’ is being reflected from various changes like the proposal to introduce Sabka Vishwas Legacy Dispute Resolution Scheme 2019 to put an end to litigations of pre- GST regime, preventing illicit import and enhanced penal provisions with an aim to ensure tax compliance.

Apart from the above, the amendments proposed in the GST law aims to remove the inherit incongruities like interest will apply only for delay in tax payment through cash, transfer of cash ledger balances, enabling provisions for new returns and creation of National Appellate Authority for Advance Ruling in case of conflicting rulings.

Overall, Budget 2019 has been an earnest attempt to bring the swaying economy back to track despite US-China meltdown."

Finance Minister Ms Nirmala Sitharaman made her budget debut in the Parliament against a back drop of a very positive Economic Survey document. At the outset this was a mixed bag covering a vast sections of the society , infra , banking , rural economy ,middle class and start ups and one could say it read as a supplement to the interim budget !

Major tax proposals made in Part B for corporates includes widening reduced corporate tax rate of 25% for corporates with annual turnover up to INR 400 crores , it was a half hearted move and the FM could have extended this to all corporates; incentive linked deduction plans for mega manufacturing plants; income tax deduction and indirect tax benefits for electric vehicles; addressing angel tax issues; benefits to start-ups like tweaking carry forward and set off of losses for start-ups; introduction of harassment free faceless e-Assessment; etc. All these are step in the right direction.

For the real estate sector under the affordable housing plan, tax holiday is proposed to be provided for profits earned by developers already existing.

As part of steps to avoid tax leverage on profit distribution by way of buy backs by listed companies, which hitherto was not covered, now brought under the relevant section.

For the individuals, although there is rebate up to INR 5 lakhs for small earners, the big earners have to bear the burden by way a high sur-charge . This practice is in fact a retrograde step as using sur- charge as a tool for revenue garnering does not augur well from a progressive Government The same applies for levying additional cess on petroleum products to augment revenue. For ease of compliance, pre-filled returns would be made available from Government sourced database. Interchangeability of PAN and Aadhar is a welcome move for individuals. These are good initiatives.

Further, the applicability of STT is now proposed to be restricted for the difference between strike and transaction price a right thing to do.

The FM has proposed strict measures and steps to discourage by way of a withholding levy on cash transactions over Rs one crore , a step in the right direction. Further prosecution proceedings are proposed to be made stronger with lower limits for trigger.

To conclude this budget did not have any bold measures how the economy is going to be transformed to become a $ 5 trillion one. Major concern is how the Government is confident of keeping the fiscal deficit target at 3.3 % and estimating a rather optimistic disinvestment target is another area of concern.

“The reforms in tax administration are commendable as it will further help in ease of doing business. However, at the same time, it needs to be seen if the faceless assessment is mandatorily or elective.

Hon’ble FM has made IFSC more lucrative by extending more tax concession and more importantly exemption from DDT and capital gains tax. Now, IFSC seems to be a go zone for investors

The buyback tax on listed companies will make buy back more costlier for listed entities. Further, it takes away the benefit of setting of losses in hands of shareholders. This proposal is effective from 5th July 2019 and it will be applicable to pending buy back transactions as well".

"Promoters and entrepreneurs can breathe easy, given that the much feared Estate Duty did not come! However, the issue is not fully closed, as the FM stated that those who are earning more should contribute more. The Finance Bill proposes to enhance the tax surcharge by 3 percentage points for those earning between Rs 2 crore and Rs 5 crore per annum, and by 7 percentage points for those earning more than Rs 5 crore. Whilst this is an additional tax burden for Corporate India’s leaders, it is still far better than an aggressive Estate Duty."

"The Indian Union Budget 2019 of NDA 2.0 has lived up-to to the expectations on boosting the Indian economy and laying the foundation for a 5 trillion USD economy. The budget stresses on physical and social infrastructure needs of the country including pollution free and has reiterated the opportunity in the infrastructure space. With focus on further opening up foreign direct investment, foreign portfolio investment and deepening of bond market, the FM has taken into account the huge capital need in the country. Inspite of allocations across sectors reflecting the priorities of the government, the fiscal deficit has been contained.

The reduced corporate tax rate of 25% would now be for companies having turnover of Rs. 400 crores thereby giving relief to around 99.3% companies. The disappointment is that this has not been reduced across the board and not extended to LLPs. Individual taxpayers have got enhanced deduction on interest for purchasing electric vehicles and affordable housing. However, the FM has not heeded to the wishes of the indivdual tax payers of removing the limit of set off existing house owners have not. To provide a non adversial tax regime, faceless assessments will be anonymous as well. Interchangeability of Aadhar and PAN will ease compliance and would also lead to widening of tax base. Certain group of taxpayers like those doing foreing travel exceeding Rs. 2 lacs, etc will be madatorily required to file ITRs, thereby helping expand the tax base. A very welcome development has been providing further exemptions and rationalizations on angel tax. The super-rich will now be taxed more with a substantial bump in surcharges leading to an maximum marginal rates of around 39% and 43% for more than Rs. 2 cr and Rs. 5 cr income earners respectively. On the international tax front, another welcome development has been rationalizations on the secondary adjustment front by paying one time tax of 18% plus srucharge 12% in case where funds cannot be brought in India.

The budget has also introduced several measures to discourage black money and promote cash less economy. An interesting development has been extending the applicability of the Black Money Act on non residents.

Overall, the budget handles the social and economic priorities well, takes steps on ease of doing business and aims to lay the platform to make India, a 5 trillion USD economy."

"Higher effective tax rates for high income earners though at first sight may seem painful yet this is in line with the global best practices. High Income earners understand this and will willingly contribute to the much needed revenues to transform India. Eventually, macroeconomics will ensure that all - the rich and the poor – benefit as India grows into an economic super power. So let’s give this proposal a chance."

"As expected – Thank You to all Tax Payers but expectation from high income earners to do be the contributors to Tax Revenues. Benefits for low income earners by way of a deduction of Rs.1.5 lakhs for interest paid on a loan taken in FY 2019-20 to buy a house for which the stamp duty value does not exceed Rs. 45 lakhs. This will be in addition to the Rs 2 lakhs interest deduction already available. In line with Green India and reducing the carbon footprint the FM has also proposed a deduction for interest paid on car loan taken to purchase an electric vehicle between 1 April 2019 and 31 March 2023.

The FM also announced implementation of faceless scrutiny assessments and moving a step closer to pre filled Income Tax Returns. High Income earners with income over 2 crores will pay taxes at an maximum marginal rate of 39% whilst those with income over 5 crores will pay maximum marginal rate of tax 42.74%. The fine print also talks about mandatory requirement to file tax returns for the following new categories of tax payers who carry out high value transactions

1. Electricity consumption bill over 1 lakh

2. Foreign travel for self or someone else over 2 lakhs or more

3. Deposit of an amount or an aggregate of the amounts exceeding Rs. 1 crore in a current account

4. Other conditions as may be prescribed

5. Persons claiming the benefits of tax exemption for long term capital gains under various provisions under section 54 of the Income Tax Act